Teaching kids about money is one of those parenting intentions that sounds simple and turns out to involve a specific set of frustrations. Cash doesn’t work the way it did when we were kids — there’s nowhere to spend it, kids don’t have it, and handing your eleven-year-old a twenty for pocket money tells them nothing about what money is or how to manage it in a world where almost everything happens on a screen.

Greenlight and GoHenry both exist to solve this problem. They both give kids a real debit card, parental controls, allowance automation, and some version of financial education built into the app. They both claim to be the best way to teach your kids money management skills.

Having used both — one with an older child who had opinions about the experience and one with a younger child who mostly cared whether they could buy things — here’s what the actual difference is.

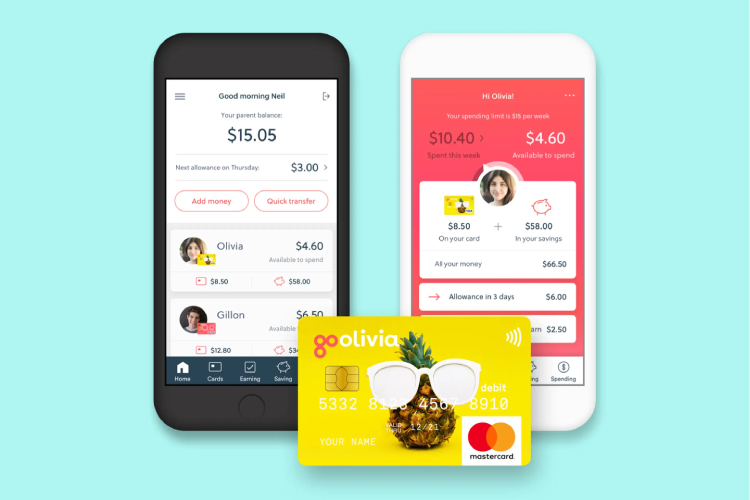

Greenlight works like this: parents create an account, add children, and transfer money to the parent wallet. From there you can allocate to each child’s spending account, savings account (with a parent-paid interest rate you set), and giving account. Kids have a physical card that works anywhere Mastercard is accepted. The parent app lets you see every transaction in real time, set spending controls by merchant category, and approve or decline transactions. The Greenlight app for kids shows their balances, their savings progress, and some financial education content depending on which subscription tier you’re on.

GoHenry works similarly. Parent account, child cards, real-time transaction visibility, parental controls. The GoHenry card is Visa. The app has spending controls and allowance automation. The GoHenry kid-facing app includes what they call Money Missions — short financial education activities that teach concepts through games and quizzes. This is GoHenry’s most distinctive feature and the one that most differentiates it from Greenlight’s approach.

If you’re buying either of these products, the card itself is not really the point. Your eleven-year-old can use a debit card from any bank. The point is whether the product actually teaches them anything about money.

GoHenry’s Money Missions are genuinely good. The activities are age-appropriate, reasonably engaging, and cover real concepts — budgeting, saving toward goals, understanding interest, the basics of earning versus spending. My older child engaged with the Money Missions more than I expected, which is a meaningful endorsement because she approaches most educational app content with visible skepticism.

The missions have a game-like structure with progress tracking, completion badges, and certificates. This works better for younger children (roughly 6-12) who respond to that kind of gamified feedback. For teenagers, the gamification can feel condescending — the completion badge for a financial literacy module doesn’t carry the same appeal at 14 that it does at 9.

Greenlight’s financial education content varies significantly by subscription tier. The basic tier doesn’t include much structured learning — it’s primarily a money management tool. The Greenlight Max tier includes investing for kids (actual fractioned shares), which is genuinely impressive as a feature and genuinely useful for teenagers who want to understand how markets work. If your goal is financial education for a teenager specifically, Greenlight Max’s investing feature is the most sophisticated offering in the children’s fintech category.

The parent-side of Greenlight is more polished than GoHenry’s. The transaction notifications arrive faster. The spending controls are more granular — you can block specific merchant categories, set per-store limits, and customize in ways that GoHenry doesn’t quite match. For parents who want detailed control over where money can be spent, Greenlight gives you more options.

The GoHenry parent experience is simpler, which is either a limitation or a feature depending on your parenting approach. The controls are sufficient for most families’ needs. The interface is cleaner in some ways because there are fewer options to navigate. The weekly money summary that arrives by email is a nice touch that keeps you aware of your child’s spending without requiring you to open the app constantly.

Both apps send real-time notifications for every transaction. Both let you transfer money immediately. Both let you automate allowance payments on whatever schedule you choose. These core functions work well in both products.

Greenlight Core: $4.99/month for up to five children.

Greenlight Max: $9.98/month, adds investing and identity theft protection.

Greenlight Infinity: $14.98/month, adds additional family features.

GoHenry: $3.99/month per child in the US. UK pricing is £3.99/month per child. This per-child pricing matters for larger families — one child is cheaper than Greenlight, two children is comparable, three children is more expensive.

The free trial periods both offer (GoHenry typically offers 1-2 months free, Greenlight offers 30 days) are worth taking advantage of before committing. These products are habit-forming in the best sense — once kids start using them and start seeing their savings grow, they become invested in the system — so the trial period tells you more than reviews do whether your specific family will engage with it.

GoHenry is better for younger children. The Money Missions structure, the simpler app interface designed for kids, and the overall experience is calibrated for 6-12 more than 13-18.

Greenlight serves a wider age range more effectively. The basic product works for younger kids. The investing feature genuinely engages older teenagers in a way that no financial education game module really does, because real money in real markets is inherently more compelling than any gamified simulation of it.

Greenlight serves a wider age range more effectively. The basic product works for younger kids. The investing feature genuinely engages older teenagers in a way that no financial education game module really does, because real money in real markets is inherently more compelling than any gamified simulation of it.

For families with children between 6 and 12 who want a structured financial education component and simple parental controls: GoHenry. The Money Missions are well-made and the product is appropriately designed for this age group.

For families with teenagers, or families with both younger and older children where investing education for the older ones is a genuine goal: Greenlight, specifically at the Max tier.

For families with three or more children where the per-child pricing comparison matters: run the numbers with your actual family size, because the math changes meaningfully at different family configurations.